Payroll for remote employees in LATAM costs 42-52% more than base salary. Employer taxes, mandatory bonuses, and severance accruals stack on top before your engineer logs a single line of code.

LATAM countries each enforce their own labor codes, statutory benefits, and payment deadlines. Mexico requires biweekly payroll runs. Brazil mandates monthly FGTS deposits equal to 8% of salary. Colombia collects cesantias by February 14 each year. A $70,000 base salary in Brazil becomes $106,400 in fully loaded annual cost.

This guide breaks down the payroll mechanics for Mexico, Brazil, Colombia, Argentina, and Peru. You will find employer tax tables, misclassification penalties by country, a side-by-side comparison of EOR vs. contractor vs. own entity, and a full breakdown of 13th-month pay and severance accruals. Use this to model your true nearshore cost before signing the first offer letter.

Why Is Payroll for Remote Employees in LATAM Different from US Payroll?

LATAM payroll operates on entirely different legal and financial assumptions than domestic US payroll. Each country’s labor code is independent, and noncompliance triggers penalties from day one.

What Do Employer Tax Burdens Look Like Across LATAM Countries?

Employer tax burdens in LATAM range from 24% to 37% above base salary before adding mandatory benefits.

| Country | Employer Tax Burden | Fully Loaded Cost Above Base | Payment Frequency |

|---|---|---|---|

| Mexico | 30-35% | 43% | Biweekly (15th/30th) |

| Brazil | 37% | 52% | Monthly |

| Colombia | 29-32% | 51% | Monthly |

| Argentina | 24-27% | 42% | Monthly |

| Peru | 30% | 44%+ | Monthly |

Mexico’s 30-35% covers IMSS social security, INFONAVIT housing fund, SAR retirement, and state payroll tax. Brazil’s 37% includes INSS, FGTS, RAT workplace accident insurance, and education levies. Colombia’s 29-32% covers pension, health, labor risk insurance, and family compensation fund. Argentina’s 24-27% covers SIPA pension, INSSJP retiree health, family allowances, and labor risk insurance.

Three planning factors matter. First, employer taxes are non-negotiable. The legal employer withholds and remits them. Missing a payment triggers penalties from day one. Second, the gap between the tax column and the fully loaded cost column represents mandatory benefits: 13th-month pay, severance funds, and vacation premiums detailed below. Third, Mexico’s biweekly cycle means 24 payroll runs per year versus 12 for Brazil, Colombia, Argentina, and Peru. That doubles your compliance touchpoints for every engineer in Mexico.

For a deeper look at hiring models that absorb these burdens, see our staff augmentation overview.

How Does Misclassification Risk Create Hidden Payroll Liabilities?

65-75% of US companies hiring internationally for the first time classify their talent as independent contractors, according to Remote.com’s 2024 Global HR Report. That classification does not survive scrutiny when the worker is a full-time, supervised software engineer.

Each LATAM country applies a substance-over-form employment test. When a worker is reclassified, liability covers the full duration of the engagement retroactively.

Mexico treats misclassification as a criminal offense. The SAT tax authority conducted over 5,000 audits targeting disguised employment in 2023. Liability includes back social security, INFONAVIT deposits, profit sharing, and severance.

Brazil has the most pro-employee labor courts in the region. Reclassification triggers five years of retroactive 13th salary, vacation bonuses, FGTS deposits at 8% of salary, and a 40% fine on accumulated FGTS at termination.

Colombia’s contrato realidad doctrine carries a penalty of one day’s salary per day of delay on severance payments.

Argentina doubles severance for unregistered employment. A senior engineer at $80,000/year with three years of tenure faces $40,000 or more in a single termination event. An EOR absorbs that liability, and our guide to hiring in Argentina through an EOR explains how registration and severance are handled.

For a senior engineer paid $80,000/year, misclassification penalties can exceed $30,000 per year of misclassification. That figure includes back taxes, social security contributions, and penalties of 20% of wages paid plus 1.5% interest, per Littler Mendelson P.C. analysis from January 2024. The US Department of Labor’s January 2024 final rule also narrowed contractor classification conditions. CTOs now face enforcement risk from both directions.

45% of companies that hire internationally already use an employer of record for at least part of their global workforce to mitigate these risks, per Velocity Global’s 2024 data.

What Payroll Deadlines Trigger Penalties When Missed?

A US company managing LATAM payroll in-house must track 12 to 24 country-specific statutory deadlines per year, per country.

Key examples by country:

- Mexico: IMSS and SAR contributions by the 17th of each month; aguinaldo by December 20; profit sharing by May 30

- Colombia: Cesantias deposits by February 14. A 10-person team with a two-week delay costs approximately 140 days of combined salary in penalties

- Brazil: 13th salary installments due November 30 and December 20

- Peru: CTS deposits semi-annually in May and November

Each deadline carries its own penalty structure. Several carry compounding daily fines.

One practical implication: managing LATAM payroll in-house requires a compliance calendar that your US finance team almost certainly does not have. Most US accounting software does not generate CTS deposit reminders or IMSS monthly close reports. You either build this infrastructure yourself or rely on a partner who already has it.

The cost of a missed deadline is not abstract. Colombia’s February 14 cesantias window is a hard cut. A team of 10 engineers with $5,000 monthly salaries that misses this deadline by two weeks owes penalties equivalent to 140 days of combined salary. That is over $93,000 in fines on a payroll that otherwise costs $50,000 per month.

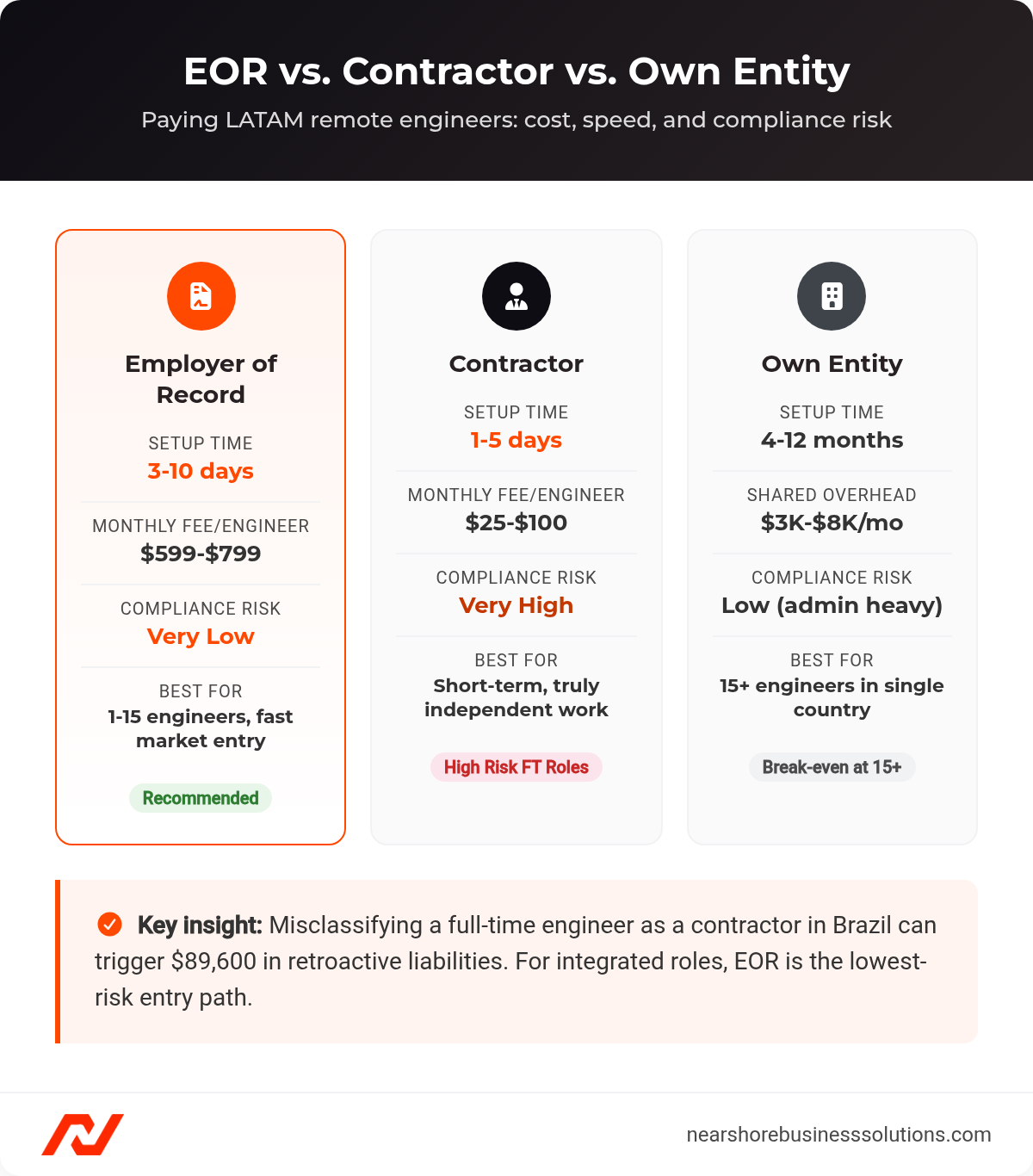

How Do You Choose Between an EOR, Contractor, or Own Entity for LATAM Payroll?

Three models exist for paying international remote employees: employer of record, contractor, and subsidiary. Each carries a different cost profile and compliance risk. Our guide to how to pay international employees compares those models across Mexico, Brazil, Colombia, Chile, and Argentina.

When Does an Employer of Record Make Sense?

An EOR gives you compliant LATAM employment in 3-10 days without incorporating a local entity. The EOR becomes the legal employer, signs the employment contract, runs payroll, remits taxes, and absorbs compliance liability. You retain full control over day-to-day work: compensation decisions, performance management, project assignments, and termination decisions.

EOR pricing has converged around $599-$799 per employee per month across Deel, Remote.com, Oyster, and Papaya Global. Velocity Global operates on custom pricing, typically $650-$850. The older percentage-of-salary model at 10-15% still exists but penalizes senior hires. A staff engineer earning $120,000 annually costs $12,000-$18,000 per year under a percentage model versus $7,188-$9,588 under a flat fee.

Hidden costs include onboarding and offboarding fees of $250-$500 per employee, currency conversion markups of 0.5-2.0% above mid-market, and off-cycle payment charges of $50-$200. A 12-person team at $699/month pays $100,692 annually in EOR fees alone.

One structural nuance to evaluate: whether the EOR operates through its own legal entities or subcontracts to local partners. Remote.com and Velocity Global emphasize owned entities, meaning the compliance chain has one fewer link. That distinction matters most during termination negotiations, labor claims, or government audits.

The EOR model works best for companies hiring 1-15 engineers in a given LATAM country, entering a new market without a legal presence, or needing an engineer productive within weeks rather than quarters.

For more on the employer of record model, see our complete EOR guide for Latin America.

What Are the Risks of Paying LATAM Engineers as Contractors?

The contractor model costs $25-$100 per month in platform fees and sets up in 1-5 days. There is no entity registration, no employer tax burden, and no statutory benefits. On the US side, you file a Form 1099-NEC, which formally documents the classification that becomes the primary exhibit in any future reclassification dispute.

Contractor status is genuinely appropriate only when all five conditions hold:

- The company defines the deliverable, not the process. No subordination.

- The engagement covers a discrete project with a defined end date.

- The contractor demonstrably serves multiple concurrent clients.

- The contractor controls their own schedule without mandated overlap hours.

- The contractor provides their own tools and infrastructure.

These criteria derive from Mexico’s Articles 20-21, Brazil’s CLT Article 3, Colombia’s Article 23, and Argentina’s Law 24.013.

The financial calculus shifts sharply over time. A contractor engagement at $8,000/month for two years generates $2,400 in total platform fees. Reclassification in Brazil would trigger approximately $89,600 in retroactive FGTS deposits, 13th salary, vacation bonuses, and INSS contributions, plus the 40% FGTS termination fine.

IP protection is also weaker under contractor status. Brazil’s copyright law defaults ownership to the creator unless a written assignment exists. Courts have scrutinized whether assignments were adequately compensated.

The contractor model remains viable for independent specialists on defined, time-bound deliverables. For full-time engineers embedded in your team for 12 months or more, the model generates compliance exposure that compounds monthly.

When Should You Set Up a Local Entity for Full Payroll Control?

Incorporating a subsidiary gives you direct control over every dimension of the employment relationship. Setup costs run $15,000-$50,000 with four to twelve months of registration and bank account opening. Ongoing accounting, legal, and administrative overhead runs $3,000-$8,000 per month.

These costs are largely fixed. They do not scale linearly with headcount. Fifteen engineers absorbing $5,000/month in shared overhead pay $333 per person, well below EOR fees. Three engineers absorbing the same overhead pay $1,667 each, nearly triple the cost of an EOR with none of the liability transfer. The break-even threshold typically falls at 10-18 employees depending on the country.

Many companies start with an EOR to validate the hiring model, then transition to a subsidiary once headcount crosses the break-even threshold.

A few country-specific notes on entity setup timelines. In Mexico, incorporating an SAS (Sociedad por Acciones Simplificada) takes roughly four to six weeks. A full SA de CV takes three to four months. In Colombia, a simplified SAS entity can register in five to ten business days, but opening a business bank account adds four to eight weeks. In Brazil, an LTDA or SA takes three to six months including tax registration across federal, state, and municipal authorities. Argentina’s SA registration averages two to three months in Buenos Aires.

These timelines matter for planning. If your first engineer in a country starts in six weeks, an EOR is your only option. Entity setup is a parallel workstream you run once you have confirmed headcount plans.

How Do EOR, Contractor, and Own Entity Compare Side by Side?

| Criteria | EOR | Contractor | Own Entity |

|---|---|---|---|

| Setup Time | 3-10 days | 1-5 days | 4-12 months |

| Monthly Cost per Employee | $599-$799 | $25-$100 | $3,000-$8,000+ (shared) |

| Compliance Risk | Very Low | Very High | Low (high admin burden) |

| IP Protection | Strong | Weaker (contract-dependent) | Strongest |

| Best For | 1-15 per country, fast entry | Short-term, truly independent | 15+ in single country |

EOR, contractor, and own entity comparison for hiring LATAM engineers: setup time, monthly fees, and compliance risk.

What Mandatory Benefits Inflate Your LATAM Payroll Budget by 20-40%?

Mandatory benefits in LATAM are statutory wage obligations enforced through the same penalty mechanisms as tax delinquency. Employees cannot waive them. Waiver clauses are void in every jurisdiction below.

What Is 13th-Month Pay and When Is It Due?

Every major LATAM market mandates at least one additional salary payment per year. These are statutory obligations, not discretionary bonuses.

| Country | Local Name | Amount | Payment Date(s) | Proration Rule |

|---|---|---|---|---|

| Mexico | Aguinaldo | Min. 15 days’ salary | By Dec 20 | 1/12 per month worked |

| Brazil | 13th Salary | 1 month’s salary | Nov and Dec installments | 1/12 per month worked |

| Colombia | Prima de Servicios | 30 days’ salary | Jun 30 and Dec 20 | Prorated for partial year |

| Argentina | SAC | 1 month’s salary | Jun 30 and Dec 18 | Prorated for partial year |

| Peru | Gratificaciones | 2 full salaries per year | July and December | Prorated by months worked |

Mexico adds a 25% vacation premium called prima vacacional on top of vacation pay. Mexico also distributes 10% of company taxable profits to employees through PTU, capped at three months’ salary. Brazil mandates a vacation bonus equal to one-third of monthly salary paid before vacation starts.

How Do Severance Accruals and Ongoing Deposits Work?

In many LATAM countries, severance is not a termination cost. It is an ongoing monthly accrual that builds throughout the employment relationship.

Brazil’s FGTS requires 8% of salary deposited monthly into a government-managed account. Upon unjust dismissal, the employer pays a 40% fine on the total accumulated balance. Colombia’s cesantias accrue at one month’s salary per year of service, deposited into a fund by February 14. The employer also pays 12% annual interest directly to the employee by January 31. Peru’s CTS deposits approximately 1.16 salaries per year semi-annually in May and November. Argentina accrues one month’s salary per year of service, with potential doubling for unregistered employment.

What Is the True Fully Loaded Cost per Country?

| Country | Base Salary (USD/mo) | Mandatory Contributions and Accruals | Total Monthly Cost | % Above Base |

|---|---|---|---|---|

| Mexico | $5,000 | $2,150 (IMSS, INFONAVIT, Aguinaldo, Prima Vacacional, PTU) | $7,150 | 43% |

| Brazil | $5,000 | $2,600 (INSS, FGTS, 13th Salary, Vacation Bonus) | $7,600 | 52% |

| Colombia | $5,000 | $2,550 (Social Security, Prima, Cesantias, Interest) | $7,550 | 51% |

| Argentina | $5,000 | $2,100 (Social Security, SAC, Severance Accrual) | $7,100 | 42% |

Fully loaded employer cost by LATAM country, including mandatory taxes and statutory benefits above $5,000/month base salary.

In a 2023 survey of 500 CFOs at US tech companies with distributed teams, 38% ranked international payroll and tax compliance as a top-three operational challenge, per Papaya Global Q4 2023 data. No US accounting system natively calculates these obligations. Each missed accrual compounds into audit liability.

Two additional costs that frequently surprise US companies: vacation pay and profit sharing. In Mexico, employees are entitled to a minimum of six days of paid vacation in year one, scaling to 12 days by year four. That vacation pay is supplemented by a 25% prima vacacional on top. PTU profit sharing distributes 10% of taxable company income across all employees annually. Companies with a handful of well-paid LATAM engineers can face a significant PTU distribution in a strong revenue year. Brazil’s vacation regime entitles employees to 30 days of paid vacation per year, plus the one-third vacation bonus paid upfront. These costs do not appear in base salary negotiations and catch many US finance teams off guard in the first year.

For salary benchmarks by role and seniority across these countries, see our LATAM salary guide.

Frequently Asked Questions About Payroll for Remote Employees

These are the most common questions CTOs and finance leaders ask when setting up LATAM nearshore payroll for the first time.

How Long Does It Take to Set Up Payroll for a LATAM Engineer?

Through an EOR, payroll setup takes 3-10 days. The EOR handles all employer registration, tax enrollment, and statutory filings. Contractor payment setup takes 1-5 days through platforms like Deel or Remote.com. Setting up your own entity takes 4-12 months depending on the country.

Do I Need to Register a Legal Entity to Hire in LATAM?

No. An employer of record handles all in-country employment obligations on your behalf. You do not need a subsidiary, a branch office, or local bank accounts to hire through an EOR. A local entity only becomes necessary when your headcount in a single country crosses 10-18 engineers, at which point the fixed costs of incorporation become cheaper than per-head EOR fees.

What Happens If I Miss a Statutory Payroll Deadline?

Penalties vary by country and deadline. Mexico’s IMSS contributions carry a daily compounding fine. Colombia’s cesantias deposit penalty equals one day’s salary for each day of delay. Brazil’s FGTS missed deposits carry interest plus a fine on the total amount due. Peru’s CTS deposits carry similar interest penalties. There is no grace period in any of these jurisdictions.

Can I Pay LATAM Engineers in USD Instead of Local Currency?

This depends on the country. Colombia and Peru allow USD-denominated contracts for contractors. For employees, most countries require payment in local currency for statutory obligations. EORs handle currency conversion and ensure local-currency compliance. When paying contractors in USD, you still absorb exchange rate risk on any dollar-to-local conversion your contractor must make.

What Is the Difference Between an EOR and a PEO for LATAM Hiring?

An employer of record becomes the legal employer of record in the country and absorbs all employment liability. A professional employer organization co-employs workers alongside your company, which requires you to have a local entity. In LATAM, EORs are the standard model for US companies without a local presence. PEOs are typically used by companies that already have a registered entity but want to outsource HR administration.

How Do I Handle Terminations for LATAM Engineers Paid Through an EOR?

You initiate the termination decision. The EOR executes the mechanics. Termination costs vary significantly by country. Argentina’s unjust dismissal cost equals one month’s salary per year of service. Brazil adds a 40% fine on the FGTS balance. Mexico requires aguinaldo proration and three months of severance for unjust dismissal. EORs typically provide a termination cost estimate before you finalize the decision.

Do LATAM Engineers Receive Equipment and Benefits the Same Way as US Employees?

Equipment is typically provided by your company, not the EOR. Benefits like health insurance are structured differently: the EOR fulfills statutory minimums (health, pension, risk insurance) that are legally required. Additional voluntary benefits like dental or supplemental health are optional and vary by EOR platform. Ask any EOR you evaluate which benefits are included in the base fee versus charged separately.

Ready to Build Your LATAM Nearshore Team?

Nearshore Business Solutions connects you with vetted software engineers from Mexico, Colombia, Argentina, and Brazil. We handle sourcing, vetting, and placement. You focus on building your product. Each candidate is pre-screened for technical skills, English fluency, and US work style fit. Our acceptance rate is 16%. Every placement includes a 90-day replacement guarantee.

Get a free consultation to discuss your nearshore payroll structure and receive a custom staffing quote.