Nearshoring tax compliance failures cost US tech companies 100-150% of total contractor payments in back taxes, fines, and legal fees. A 2023 KPMG survey found 41% of US executives cite navigating foreign tax laws as a significant challenge with nearshore engagements.

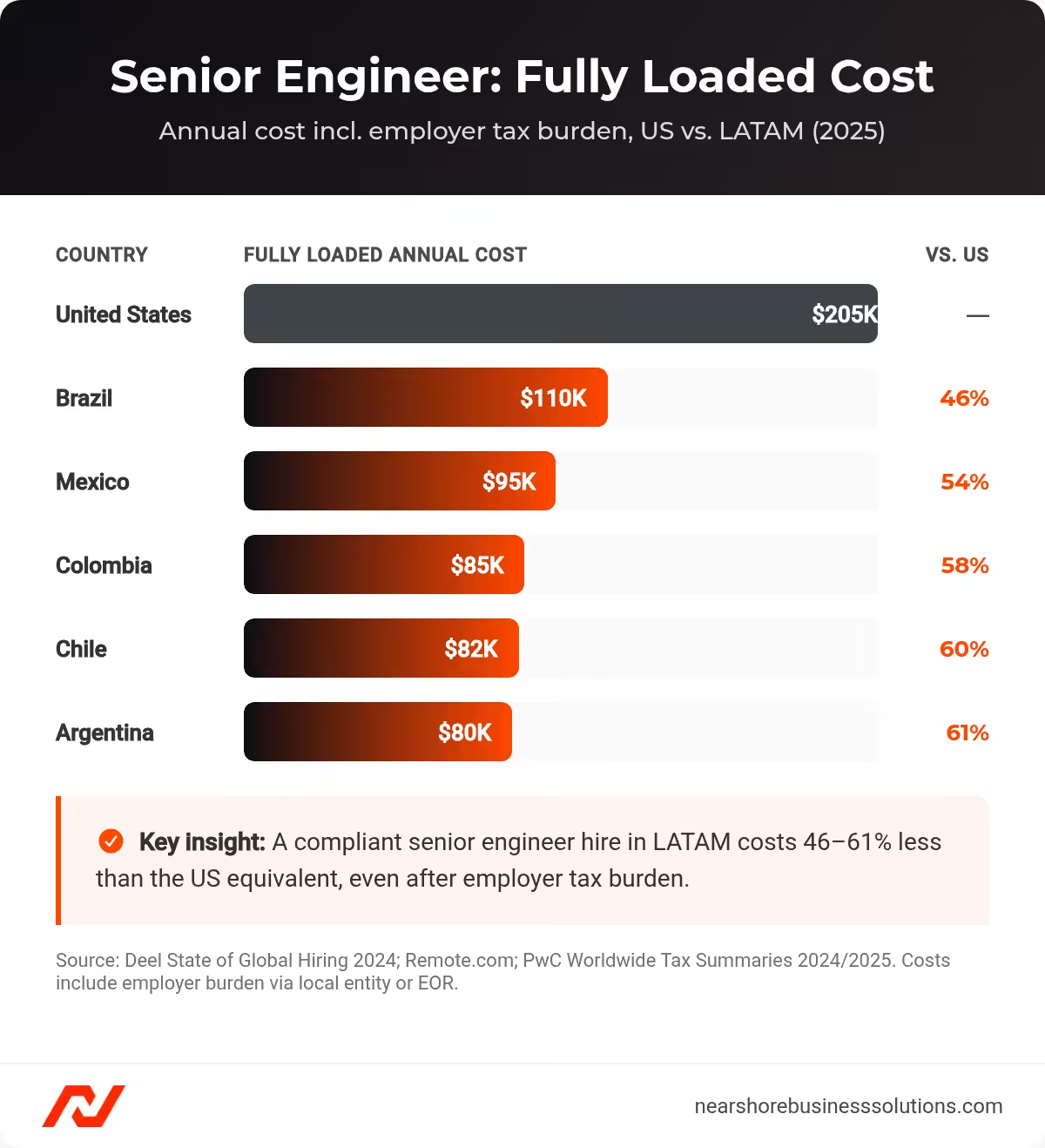

LATAM senior engineers cost $80,000-$110,000 fully loaded per year versus $205,000 in the US. But three failure modes erase those savings: worker misclassification, permanent establishment triggers, and unbudgeted withholding taxes. Companies operating through an Employer of Record in Latin America avoid all three.

This guide covers country-by-country tax rates, misclassification penalties, currency costs, and the compliance structure that protects your savings. You’ll find data from KPMG, PwC, Deloitte, the OECD, and national tax authorities for Brazil, Mexico, Colombia, Argentina, and Chile through 2025-2026.

Why Does Nearshore Tax Compliance Fail for U.S. Companies?

Three failure modes cause most nearshore compliance damage. Misclassifying employees as independent contractors is the most common. Triggering a permanent establishment without realizing it is the most expensive. Ignoring withholding tax obligations is the most silent. Financial exposure from a single misclassification event can exceed 100-150% of total payments made to the worker over a two-to-five year audit period.

What Makes Worker Misclassification So Costly in Latin America?

Misclassification triggers five financial consequences simultaneously. Mexico’s post-2021 reform sets administrative fines at MXN 250,000 to MXN 5,000,000 (approximately USD 14,000 to USD 280,000) per affected worker.

The five simultaneous costs:

- Retroactive statutory benefits: 13th-month salary, vacation bonuses, severance fund contributions backdated to original engagement start

- Employer-side social security contributions: plus interest and inflation adjustments that in Argentina can multiply the original obligation by 3-5x

- Administrative fines per worker: Mexico sets these at MXN 250,000 to MXN 5,000,000 per worker

- Litigation costs and labor court awards: including moral damages in cases of deliberate structuring

- US-side IRS penalties: for failure to file proper foreign contractor reporting on Forms 1099 and W-8BEN

Misclassification risk runs on two parallel tracks. On the US side, the IRS applies its common law test (IRS Publication 15-A), creating liability for unpaid FICA and FUTA taxes, plus Section 3509 penalties. On the LATAM side, labor authorities apply the “primacy of reality” doctrine. The written contract is secondary to the actual working relationship. If your contractor attends daily standups, uses your Jira board, and reports to your engineering manager, LATAM courts will classify that person as an employee regardless of what the contract says.

| Country | Trigger | Financial Outcome |

|---|---|---|

| Brazil (2022) | Single developer on a 15-person contractor team filed a labor court claim. All 15 participated in Agile sprints, used company Slack and Jira, reported to a US-based manager. | Five years of retroactive FGTS, INSS, 13th salaries, and vacation pay totaling over USD $1.2 million. |

| Mexico (2023) | STPS audited a US fintech using a local staffing agency for core engineering after the 2021 reform. | Joint fines exceeding MXN 4 million plus mandatory order to recognize engineers as direct employees with retroactive benefits recalculation. |

| Argentina (2021) | Single contractor sued for misclassification despite explicit independent contractor contract. | Severance award reached multiples of annual compensation, indexed for hyperinflation. |

When Does a Remote LATAM Team Create Permanent Establishment?

A permanent establishment (PE) transforms your remote LATAM team into a taxable corporate presence in that country. Your US company must then pay local corporate income tax on profits attributable to that activity. Three trigger mechanisms create exposure under the OECD Model Tax Convention Article 5.

Fixed place of business PE. Workers operating from a co-working space, or from their homes in a coordinated manner, can constitute a de facto office. The 2017 OECD commentary expanded this definition materially. No lease agreement or signage is required.

Misclassification-triggered PE. If contractors are deemed employees performing core business functions, the OECD framework treats that team as a fixed place of business. The US company owes corporate income tax on attributable profits, layered on top of all employment-related back taxes. One compliance failure triggers two independent liability streams.

Agency PE (Article 5(5)). A person who habitually concludes contracts on behalf of a foreign enterprise can independently create PE, even without a fixed office. A senior LATAM engineer who signs vendor agreements or commits to client deliverables can cross this threshold.

What Currency and Repatriation Costs Should You Budget For?

Cross-border payment mechanics add 5-20% in hidden costs that rarely appear in initial hiring budgets. Three countries carry the highest risk.

Argentina. The CEPO Cambiario (capital controls) creates an official-to-parallel rate gap that has historically exceeded 50-100%. Paying employees at the official rate effectively cuts their real-world compensation in half. Companies cannot simply wire USD to Argentine local bank accounts. Estimated cost adder: 40-80% above headline labor costs.

Brazil. The IOF (financial transactions tax) applies automatically on every cross-border payment at FX conversion. BRL/USD exhibited approximately 10-15% annual volatility in 2023. A developer hired at BRL 25,000/month can cost 10-15% more or less in USD terms within a single quarter. Estimated cost adder: 5-15%.

Colombia. Withholding on outbound service payments to non-residents runs 15-20%. If the US company cannot credit that amount against US tax liability, it becomes a pure cost adder. Estimated cost adder: 5-10%.

What Does Nearshoring Tax Compliance Require Country by Country in 2025-2026?

LATAM senior engineers save US companies 46-61% versus US fully loaded costs, but only when engaged through a compliant structure. The country-by-country breakdown below shows the tax rates, withholding rules, and 2025-2026 updates that affect your actual cost. For companies evaluating structure options, see our EOR vs. local entity comparison for Latin America.

How Do LATAM Tax Rates Compare Across Countries?

LATAM corporate tax rates range from 27% (Chile) to 35% (Colombia, Argentina). Withholding on services paid to non-residents ranges from 15% to 31.5%.

| Country | Corporate Tax | Withholding on Services | PE Threshold | 2025-2026 Key Update |

|---|---|---|---|---|

| Brazil | 34% | 15-25% | Dependent agent, fixed place, habitual contract execution | Transfer pricing OECD alignment enforced; LGPD escalation |

| Mexico | 30% | 25% (reducible via treaty to 10%) | Dependent agent, fixed place, 183-day service PE | PTU cap enforcement; minimum wage threshold impacts |

| Colombia | 35% | 15-20% | Fixed place, dependent agent, 183-day threshold | Digital nomad visa tax residency triggers |

| Argentina | 35% | 21-31.5% | Dependent agent, fixed establishment | FX control evolution; Ley de Economia del Conocimiento |

| Chile | 27% | 15-20% | Fixed place, dependent agent | 40-hour workweek phase-in by 2028 |

Critical treaty note: The US-Brazil tax treaty signed in 2023 remains unratified. No treaty benefits are available. The US-Chile treaty (in force late 2023) actively reduces withholding on qualifying technical services. The US-Mexico treaty can eliminate withholding on independent personal services entirely, provided the contractor maintains no fixed base in the US.

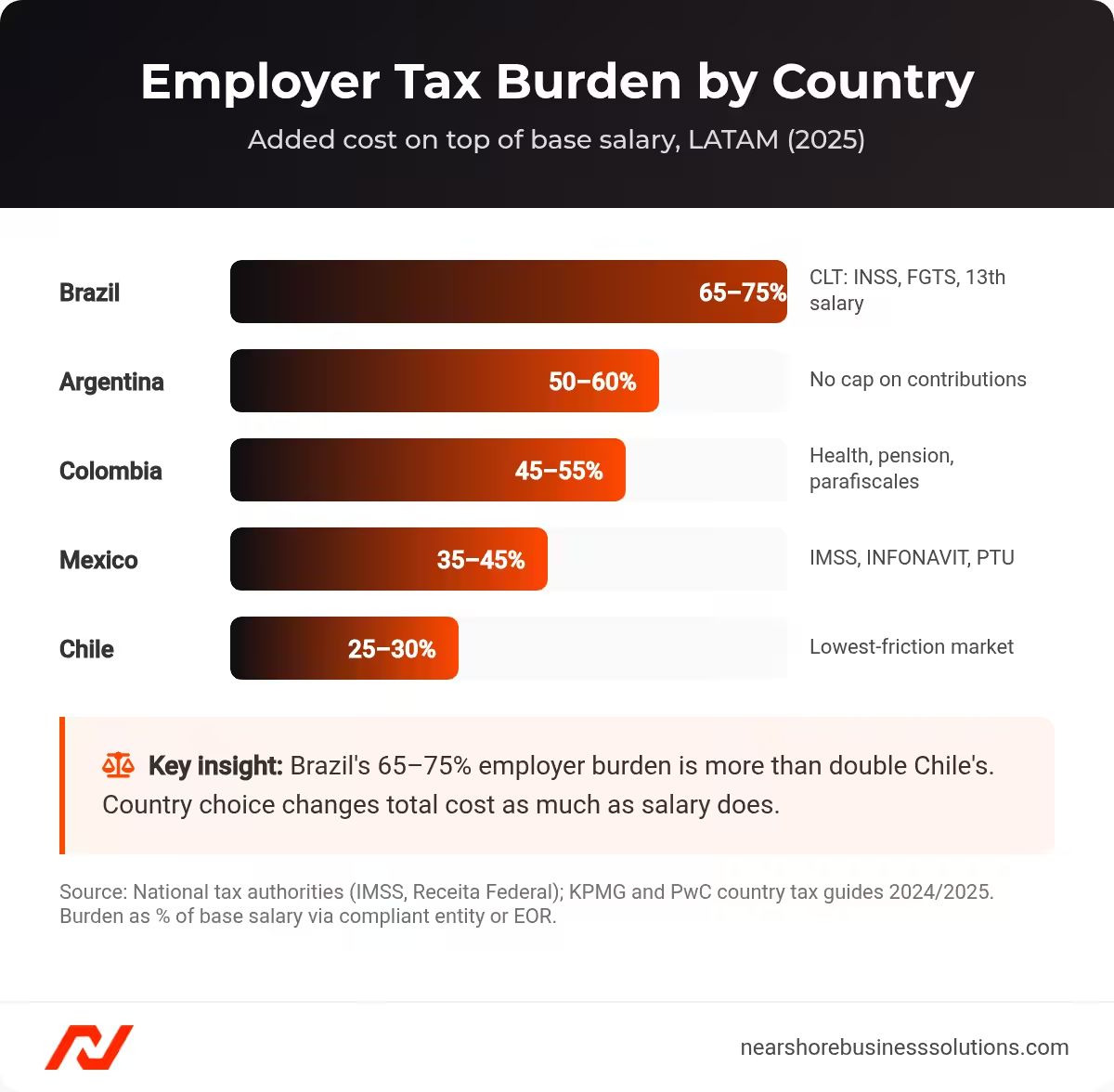

Employer tax burden as a share of base salary across five LATAM countries in 2025.

What Is the Fully Loaded Cost of a Senior Engineer in Each LATAM Country?

A senior software engineer (5-8 years experience) costs $80,000-$110,000 per year fully loaded in LATAM versus $205,000 in the US. Brazil carries the highest employer burden at 65-75%. Chile carries the lowest at 25-30%.

| Country | Median Net Salary | Employer Burden | Est. Fully Loaded Annual Cost | Savings vs. US |

|---|---|---|---|---|

| United States | $155,000 | 18-22% | $205,000 | — |

| Mexico | $65,000 | 35-45% | $95,000 | 54% |

| Brazil | $60,000 | 65-75% | $110,000 | 46% |

| Colombia | $55,000 | 45-55% | $85,000 | 58% |

| Argentina | $50,000 | 50-60% | $80,000 | 61% |

| Chile | $62,000 | 25-30% | $82,000 | 60% |

Fully loaded senior engineer cost across the US and five LATAM countries, with savings versus US rates.

Source: Salary data from Deel State of Global Hiring Report 2024 and Remote.com Global HR Data. Employer burden from PwC Worldwide Tax Summaries 2024/2025.

These numbers assume compliant engagement through a local entity or EOR. Engaging the same talent as independent contractors eliminates the employer burden line, but transfers the full misclassification liability onto your balance sheet.

What Are Brazil’s CLT, LGPD, and Transfer Pricing Requirements?

Brazil combines the region’s largest talent pool with its heaviest compliance load. The CLT prescribes employer-side costs at 65-75% of base salary. These cannot be negotiated or deferred.

CLT employer obligations (2025 rates):

- INSS (Social Security): 20-23% of payroll (20% flat plus 1-3% occupational risk surcharge)

- FGTS (Severance Fund): 8% of monthly salary deposited into a government-administered blocked account

- 13th Salary: 8.33% of annual salary, paid in two installments, with INSS and FGTS applying on top

- Vacation plus 1/3 Bonus: 11.1% of annual salary, plus employer contributions on vacation pay

- Meal and Food Vouchers: BRL 600-1,200 per month. Collective bargaining agreements in tech universally require them.

- Combined employer burden: 65-75% on top of base salary

Termination cost multiplier: Dismissal without cause triggers a 40% penalty on accumulated FGTS. For a three-year senior engineer, this single penalty can exceed USD $15,000.

Withholding on cross-border payments: Payments to Brazilian independent contractors for technical services are subject to 15% IRRF withholding tax plus 10% CIDE (Contribution for Intervention in the Economic Domain). The US-Brazil tax treaty signed in 2023 remains unratified as of 2026. No treaty benefits are currently available to reduce these rates.

LGPD: US companies processing Brazilian worker data must establish a valid legal basis under Brazil’s data protection law (Lei 13,709/2018). Fines reach up to 2% of Brazil revenue, capped at BRL 50 million per violation. The ANPD moved to active sanctions in 2023. Companies using EORs remain joint controllers if they access performance metrics, code reviews, or Slack messages containing personal information.

Transfer Pricing (Law 14,596/2023): Brazil’s new OECD-aligned arm’s-length pricing rules are fully enforced by 2026. They require functional analysis, benchmarking studies, and proactive documentation for intercompany transactions. Companies that previously used Brazil’s fixed-margin system must restructure by 2026 or face adjustment assessments with compound interest.

What Compliance Requirements Apply Under Mexico’s Post-Outsourcing Reform?

Mexico’s 2021 reform banned subcontracting personnel for core business activities. For a US software company, a Mexican staffing agency supplying engineers to write production code is precisely what was prohibited. The reform created “illegal simulation of employment” as a specific prosecutable category. Only two compliant structures survive.

Compliant structures:

- An EOR acting as the legal employer (not a staffing intermediary)

- A local subsidiary with direct hires

All specialized service providers must register with REPSE. Unregistered providers face automatic fines.

Mexico employer obligations (2025 rates):

| Obligation | Rate | Key Notes |

|---|---|---|

| IMSS (Social Security) | 20-25% | Complex bracket system on integrated daily wage |

| INFONAVIT (Housing) | 5% | Cannot be offset or deferred |

| SAR (Retirement) | 2% in 2025, rising to 13.875% by 2030 | Holding at 2% understates future costs by up to 6x |

| ISN (Payroll Tax) | 2-3% | State-level, varies by location |

| PTU (Profit Sharing) | 10% of taxable profit | Capped per employee, can still reach USD $5,000-$15,000 annually |

Contractor option: Mexico’s RESICO simplified tax regime offers 1-2.5% income tax rates for individuals earning up to MXN 3.5 million annually (approximately USD 200,000). This makes contracting attractive, but only when genuine independence exists. The STPS continues auditing arrangements since the 2021 reform.

US-Mexico treaty advantage: The US-Mexico tax treaty generally reduces or eliminates withholding tax on payments for independent personal services, provided the contractor does not have a fixed base in the US. This is a material cost advantage versus Brazil, where no treaty protection is currently available.

Guadalajara and Monterrey represent Mexico’s two primary tech hubs. Guadalajara, often called Mexico’s Silicon Valley, produces graduates from Tecnologico de Monterrey (ITESM) and UNAM each year. Monterrey hosts a major enterprise software cluster. Both cities offer 1-3 hour timezone overlap with all US regions. When STPS audits occur, they most commonly target companies sourcing engineering talent from these two markets through non-compliant staffing arrangements.

What Are the Key 2026 Compliance Issues in Colombia, Argentina, and Chile?

Colombia, Argentina, and Chile each carry distinct compliance risks entering 2026. Colombia’s digital nomad visa creates PE exposure. Argentina’s currency controls add 40-80% to headline costs. Chile offers the region’s lowest employer burden at 25-30%.

Colombia: Employer contributions total 45-55% of base salary. That breaks down as health 8.5%, pension 12%, ARL 0.522-6.96%, parafiscales 9%, plus prima de servicios and cesantias. The 2022 tax reform (Law 2277) modified withholding thresholds on non-resident payments. Digital nomad visa holders who spend 183 or more days in Colombia become tax residents with worldwide income taxation. This potentially generates PE exposure for US companies whose team members hold this visa.

Argentina: Employer social security contributions total 23-27% of gross salary with no cap. This makes high-salary engineering roles disproportionately expensive. The Ley de Economia del Conocimiento provides qualifying companies a 60% reduction in employer contributions through 2029, potentially cutting the burden to 9-11%. Monotributo registration provides partial misclassification protection, but courts have reclassified monotributistas as employees when subordination evidence is present. DNU 70/2023 labor deregulation provisions remain subject to judicial injunctions. Do not rely on them until definitively resolved. Companies like Globant and MercadoLibre operate through local subsidiaries to maintain full compliance.

Chile: The lowest-friction market at 25-30% employer burden. Independent contractors issue boletas de honorarios through the SII platform. Clients must withhold 13.75% (rising to 17% by 2028) as provisional income tax. The 40-hour workweek phases in through 2028: 44 hours from April 2024, 42 hours from April 2026, 40 hours from April 2028. The Direccion del Trabajo has increased inspections of boleta arrangements in tech since 2023.

The US-Chile tax treaty (in force since late 2023) actively reduces withholding on qualifying technical services. This is one of the few LATAM countries where treaty benefits are currently available to US companies, making Chile uniquely cost-effective for both employment and contractor structures. Santiago hosts the majority of Chile’s tech sector, with strong English proficiency and direct flight connections to Miami, Houston, and New York.

Summary: Which country fits which compliance strategy? Chile is best for simple contractor arrangements thanks to the boleta system and US treaty. Mexico is optimal for compliant EOR employment at the highest savings rate (54%). Colombia offers the best cost-to-compliance balance for companies wanting a direct subsidiary. Brazil and Argentina require the most compliance infrastructure but offer the largest talent pools for specialized engineering roles.

Frequently Asked Questions About Nearshore Tax Compliance

These are the most common questions CTOs and finance leads ask about nearshore tax compliance in Latin America.

Do U.S. Companies Need a Local Entity to Hire in Latin America?

No, you do not need a local entity. An Employer of Record handles legal employment on your behalf without requiring you to register a subsidiary. The EOR is the legal employer in the LATAM country, manages all tax filings and benefits, and you pay the EOR a service fee. Setting up a local entity takes 30-90 days and requires ongoing compliance overhead. An EOR can onboard workers in as few as 3-7 days.

What Is the Safest Way to Pay LATAM Contractors?

The safest structure is employment through an EOR rather than contractor engagement. If you use contractors, verify genuine independence exists: the worker sets their own hours, uses their own tools, and works for multiple clients. Mexico’s RESICO regime and Chile’s boleta de honorarios both provide partial legal clarity, but neither eliminates misclassification risk if your working relationship resembles employment.

How Does Permanent Establishment Risk Affect Remote Teams?

PE risk applies when your LATAM team performs core business functions from a fixed location, when someone habitually signs contracts on your behalf, or when the team collectively operates like a fixed office. PE triggers corporate income tax on attributable profits in the LATAM country, independent of any misclassification liability. Using an EOR eliminates PE risk because the EOR is the legal employer and the fixed establishment in that country.

What Happens If a LATAM Contractor Files a Labor Claim?

Labor courts in Brazil, Mexico, Colombia, Argentina, and Chile all apply the primacy of reality doctrine. If the actual working relationship resembles employment, the court will reclassify the worker regardless of what the contract says. You will owe retroactive benefits, social security contributions, and statutory severance for the full engagement period, plus fines and interest. The exposure period is typically two to five years.

Is Brazil Worth the Compliance Complexity?

Brazil carries the region’s highest employer burden at 65-75%, the heaviest data protection obligations under LGPD, and new OECD-aligned transfer pricing rules enforced from 2026. It also has the largest talent pool in Latin America and strong senior engineering depth in fintech, e-commerce, and enterprise software. Most US companies operating at scale in Brazil use an EOR or a fully established subsidiary to absorb the compliance load. The cost savings at 46% below US rates still justify the complexity for the right team size.

How Do I Handle Currency Risk in Argentina?

Argentina’s CEPO Cambiario (capital controls) prevents direct USD wire transfers to local bank accounts. Companies pay through EOR providers who handle peso conversion, or use structured payment mechanisms like MEP (Mercado Electronico de Pagos). Budget 40-80% above headline labor costs to account for FX gaps, inflation indexing, and compliance overhead. The Ley de Economia del Conocimiento provides qualifying tech companies a 60% employer contribution reduction, which partially offsets currency costs.

What Reporting Does the IRS Require for LATAM Contractors?

US companies must file Form 1099-NEC for payments to US persons and must collect Form W-8BEN from foreign contractors to certify their non-US status. Failure to collect W-8BEN can trigger backup withholding at 24% on all payments. For employees hired through an EOR, the EOR handles local payroll tax filings. The US company’s reporting obligation is limited to the service fee paid to the EOR.

Ready to Build a Compliant LATAM Engineering Team?

Nearshore Business Solutions sources and vets engineers from Mexico, Colombia, Brazil, Argentina, and Chile. We screen for technical skills, English fluency, and US work-style fit. Our acceptance rate is 16%.

Every placement includes a 90-day replacement guarantee. You receive pre-vetted candidates in 2-4 weeks.

Get a free compliance consultation to discuss your LATAM hiring structure and receive a custom EOR or staff augmentation quote.